All Categories

Featured

Table of Contents

When you gain passion in an annuity, you generally do not need to report those incomes and pay income tax on the profits every year. Growth in your annuity is protected from individual revenue tax obligations.

While this is an introduction of annuity tax, speak with a tax obligation specialist before you make any kind of choices. Lifetime annuities. When you have an annuity, there are a variety of information that can impact the tax of withdrawals and income repayments you obtain. If you place pre-tax money right into a specific retirement account (IRA) or 401(k), you pay tax obligations on withdrawals, and this is true if you money an annuity with pre-tax money

If you have at least $10,000 of profits in your annuity, the entire $10,000 is dealt with as income, and would commonly be taxed as average income. After you exhaust the profits in your account, you obtain a tax-free return of your original swelling sum. If you convert your funds into a guaranteed stream of earnings payments by annuitizing, those settlements are split into taxable sections and tax-free portions.

Each settlement returns a portion of the cash that has actually currently been taxed and a part of interest, which is taxed. As an example, if you get $1,000 per month, $800 of each settlement may be tax-free, while the staying $200 is taxable earnings. At some point, if you outlive your statistically identified life expectations, the entire amount of each settlement might end up being taxable.

Since the annuity would certainly have been moneyed with after-tax money, you would not owe tax obligations on this when withdrawn. In general, you must wait up until at the very least age 59 1/2 to take out earnings from your account, and your Roth needs to be open for at least 5 years.

Still, the various other attributes of an annuity might surpass revenue tax treatment. Annuities can be devices for deferring and handling tax obligations.

How does Annuity Withdrawal Options inheritance affect taxes

If there are any type of penalties for underreporting the revenue, you could be able to ask for a waiver of charges, but the rate of interest generally can not be waived. You could be able to set up a layaway plan with the internal revenue service (Annuity interest rates). As Critter-3 stated, a neighborhood expert may be able to assist with this, but that would likely lead to a little additional expense

The original annuity agreement holder should include a death benefit provision and name a recipient. Annuity recipients are not limited to individuals.

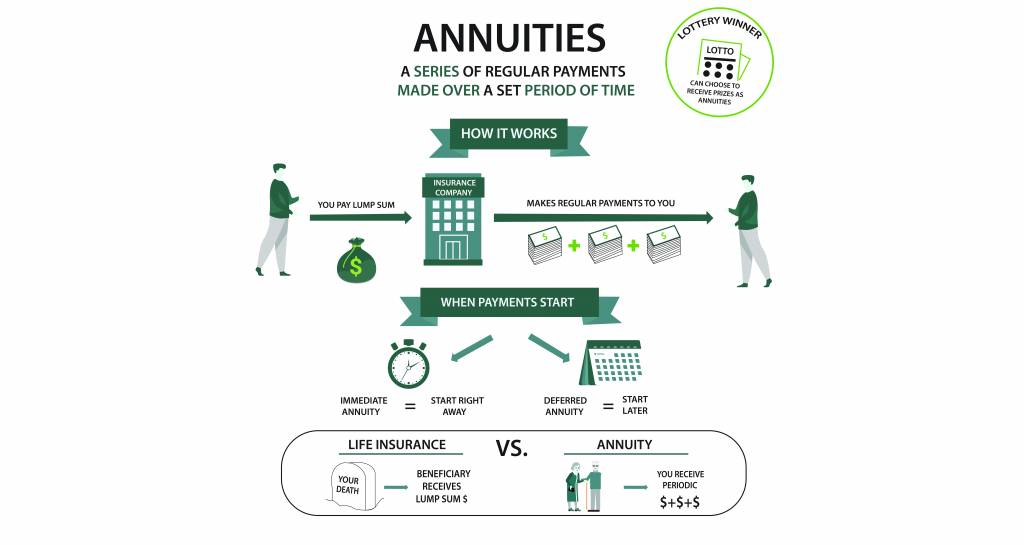

Fixed-Period Annuity A fixed-period, or period-certain, annuity ensures settlements to you for a details length of time. Settlements may last 10, 15 or 20 years. If you pass away throughout this time around, your picked beneficiary receives any kind of staying payments. Life Annuity As the name recommends, a life annuity warranties you repayments for the remainder of your life.

What taxes are due on inherited Joint And Survivor Annuities

If your contract consists of a fatality benefit, staying annuity repayments are paid out to your beneficiary in either a round figure or a series of payments. You can select someone to get all the offered funds or several individuals to get a percent of staying funds. You can likewise choose a not-for-profit organization as your recipient, or a trust established as component of your estate plan.

Doing so enables you to keep the very same options as the initial owner, including the annuity's tax-deferred status. Non-spouses can likewise inherit annuity settlements.

There are 3 primary means recipients can receive acquired annuity payments. Lump-Sum Distribution A lump-sum distribution permits the recipient to receive the agreement's whole continuing to be value as a solitary settlement. Nonqualified-Stretch Arrangement This annuity agreement condition permits a beneficiary to get settlements for the rest of his/her life.

In this situation, tax obligations are owed on the entire difference in between what the initial owner paid for the annuity and the fatality benefit. The swelling amount is exhausted at average revenue tax rates.

Spreading settlements out over a longer period is one method to avoid a large tax bite. For instance, if you make withdrawals over a five-year duration, you will certainly owe taxes just on the increased worth of the section that is withdrawn in that year. It is likewise much less most likely to push you right into a much greater tax bracket.

Are Retirement Annuities death benefits taxable

This provides the least tax exposure but additionally takes the lengthiest time to receive all the money. Annuity contracts. If you've inherited an annuity, you typically should make a decision concerning your survivor benefit swiftly. Decisions about exactly how you wish to get the cash are typically final and can't be changed later on

An acquired annuity is a financial item that allows the recipient of an annuity contract to proceed receiving repayments after the annuitant's fatality. Inherited annuities are commonly utilized to supply income for enjoyed ones after the fatality of the key breadwinner in a family. There are two kinds of inherited annuities: Immediate inherited annuities start paying today.

Are Annuity Beneficiary death benefits taxable

Deferred acquired annuities allow the recipient to wait up until a later date to begin obtaining repayments. The most effective thing to do with an inherited annuity depends upon your financial scenario and needs. A prompt acquired annuity might be the best choice if you need immediate revenue. On the various other hand, if you can wait a while before starting to get payments, a deferred inherited annuity may be a better choice. Joint and survivor annuities.

It is very important to speak with an economic consultant prior to making any kind of decisions about an acquired annuity, as they can help you identify what is best for your private circumstances. There are a couple of risks to consider prior to spending in an acquired annuity. First, you should recognize that the federal government does not assure acquired annuities like various other retired life products.

Tax treatment of inherited Annuity Withdrawal Options

Second, acquired annuities are frequently complex financial products, making them challenging to comprehend. There is always the risk that the worth of the annuity can go down, which would reduce the quantity of cash you get in payments.

{kind=link}

Table of Contents

Latest Posts

Breaking Down Your Investment Choices A Comprehensive Guide to Investment Choices What Is Annuity Fixed Vs Variable? Pros and Cons of Variable Vs Fixed Annuity Why Variable Annuity Vs Fixed Annuity Is

Analyzing Strategic Retirement Planning Key Insights on Fixed Vs Variable Annuity Pros Cons Defining the Right Financial Strategy Features of Smart Investment Choices Why Choosing the Right Financial

Exploring Fixed Vs Variable Annuity Pros And Cons Key Insights on Fixed Vs Variable Annuity What Is Variable Annuities Vs Fixed Annuities? Pros and Cons of Fixed Vs Variable Annuities Why Choosing the

More

Latest Posts